Omnibus: Key Takeaways

What does the Omnibus mean for private investors and their portcos?

Omnibus on Sustainability Reporting: Key Takeaways

The day has arrived, on the 24 February 2026, the EU adopted the Omnibus Directive on Sustainability Reporting. This directive aims to simplify and amend the rules of the main instruments in this field (with the exception of the SFDR):

- The CSRD,

- CS3D and

- EU Taxonomy.

The Omnibus was divided into two initiatives:

- One proposing to delay mandatory sustainability reporting by two years, adopted in April 2025.

- One proposing to reduce the scope and datapoints of the reports, just adopted.

With the adoption of the second initiative, the first one lost all its relevance, given that the delays turned into exemptions: the companies left out of scope will not have to report.

How do the Omnibus changes affect Fund Managers?

Directly, they don't. Financial entities must comply with the SFDR, which remains unchanged.

Nevertheless, it is extremely relevant for Article 9 funds, specifically funds that invest in sustainable objectives aligned with the EU Taxonomy. Assessing Taxonomy alignment will be easier and render more positive results, given the possibility to report partial alignment. We will explain this point more in depth below.

The datapoint reduction is expected to make CSRD disclosures more aligned with SFDR indicators. This not only would make it less burdensome for companies to comply with CSRD requirements, but also for Fund Managers to take a pragmatic approach to ESG reporting, conducting one data collection exercise for their entire portfolio at the same time as they gather their own SFDR data.

Lastly, beyond the legal perspective, the AFM has highlighted some practical consequences of the Omnibus on investors. In essence, the lowered reporting requirements will lead to a decrease in the amount of ESG data publicly available for investors to rely on.

We will now outline the main changes introduced by the Omnibus and the key takeaways we can derive from them for each directive.

CSRD

Below is an overview of the main changes in scope for the CSRD.

Scope reduction

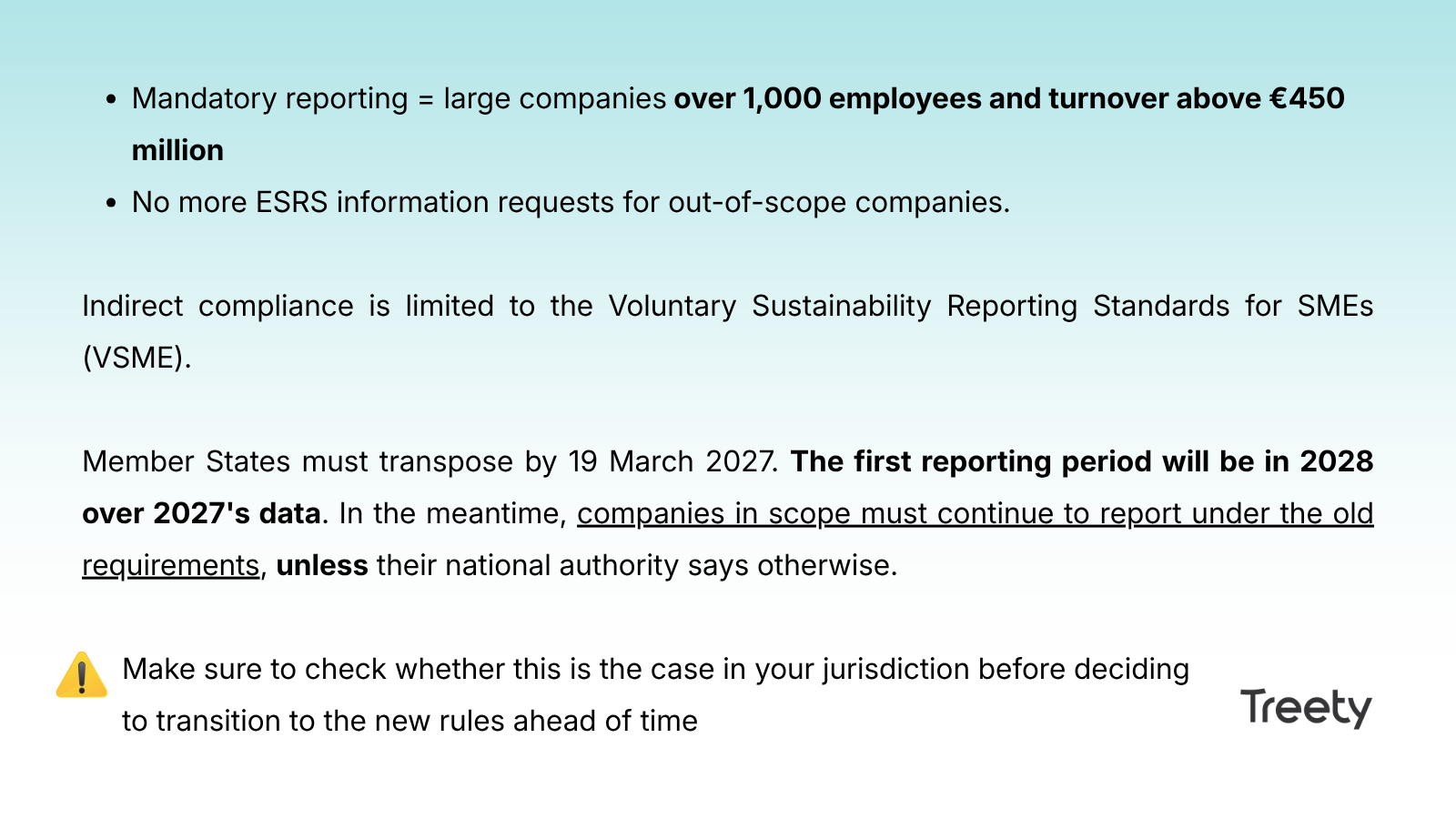

Mandatory reporting is now limited to large companies over 1,000 employees and turnover above ‚ 50 million or a balance sheet above ‚ 25 Million.

Under the current rules, the first wave encompasses large companies above 500 employees and subject to the NFRD. The revised scope entails an 80% reduction in the number of companies in scope for the first wave.

This is actually a step back not just to before the CSRD was enacted, but even further backwards, since this scope is even smaller than that of the former NFRD.

No more indirect reporting

Under the amendments, out-of-scope companies will no longer be required to provide full ESRS information to in-scope companies, effectively suppressing indirect compliance to ease the burden on SMEs.

The data requests will be limited to 20 datapoints, those established under the Voluntary Sustainability Reporting Standards for SMEs (VSME) framework. These are also the standards suggested by the Commission for companies who still wish to report voluntarily under a less burdensome framework.

In our view, it may fall short in some cases. Check this article to understand why the LSME could be a better alternative for voluntary reporting.

If you already set up processes to collect the ESRS datapoints, it may be beneficial to keep them in place for future transparency and as a competitive advantage. That said, if gathering the data was truly disproportionate and burdensome, the amended rules would no longer oblige you to do so.

Datapoints reduction

The Commission further announced a reduction of ESRS, prioritising quantitative over narrative datapoints and making some disclosures voluntary. These amendments to the ESRS will be done through a delegated act, expected to be published in October 2025.

Companies expecting a new set of sector-specific ESRS can also set those expectations aside. The Proposal revokes the Commission mandate to adopt such standards.

EU Taxonomy

Below is an overview of the main changes in scope for the EU Taxonomy:

Scope reduction

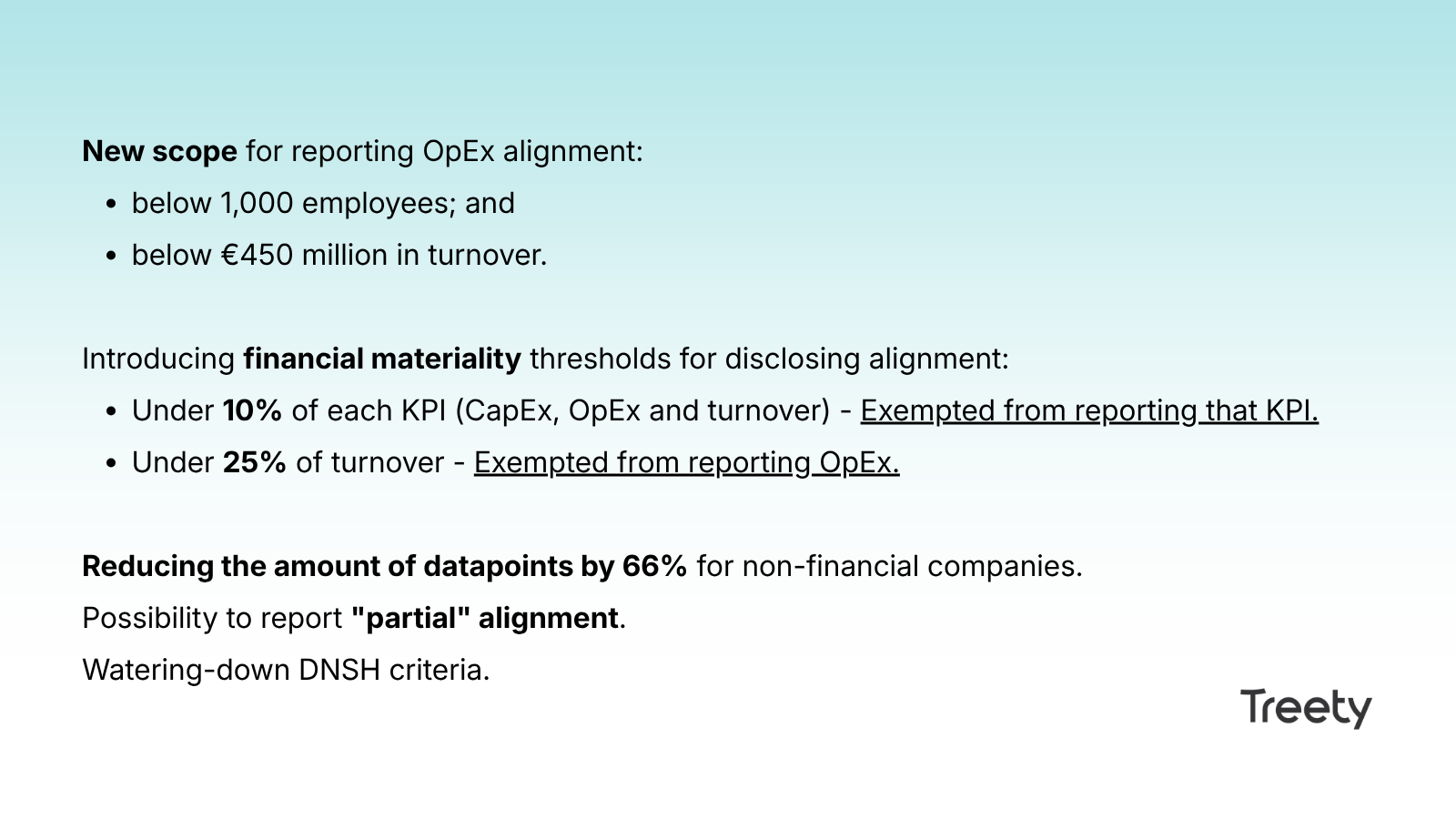

The Proposal introduces an exemption from assessing full alignment for undertakings below 1,000 employees and ‚ 450 million in turnover. These companies will be exempted from disclosing OpEx alignment.

The Commission calls it an opt-in approach: companies under 1,000 employees must only disclose OpEx alignment if they wish to claim that those activities are sustainable.

While the Commission argues that OpEx alignment has less informational value and decision usefulness, in certain cases, OpEx disclosures can be highly revealing and worth considering voluntarily. When a company is phasing in green initiatives, OpEx (e.g., on renewable energy procurement, circular economy initiatives, or supplier engagement programs) can indicate real steps toward sustainability before larger investments show up in CapEx.

Another example is that of businesses in services, SaaS, consulting, or finance, which often have lower CapEx but significant sustainability-related OpEx.

Introducing financial materiality thresholds

The Omnibus also excludes alignment assessments for activities that are not considered material from a financial standpoint. There is a presumption of lack of materiality if:

- The KPI (turnover, CapEx or OpEx) is below 10%, companies will be exempted from disclosing alignment with that particular KPI.

- If the turnover of a certain activity is below 25%, companies will also be exempted from disclosing OpEx alignment.

Datapoint reduction

The Proposal announced a 66% datapoint reduction for non-financial entities. Therefore, activities must meet lower Technical Screening Criteria (TSC) to report alignment with the EU Taxonomy.

Companies are moreover allowed to report partial alignment. That is, if an activity complies with some but not all TSC, companies will be allowed to disclose that their activity is partially sustainable.

Lastly, Do No Significant Harm (DNSH) criteria will be substantially reduced, in particular those in Appendix C, concerning chemical substances.

CS3D

The CS3D or CSDDD primarily impacts a small group of very large companies and therefore is not as relevant for most investors and mid-sized businesses. We will briefly outline the most significant updates.

Among the proposed amendments, due diligence obligations will be limited to direct business partners and relevant stakeholders. Where under the current rules companies have to look deep into their value chain, these assessments will be restricted to tier one suppliers, distributors and other stakeholders. And, similarly to the CSRD, out-of-scope companies will also no longer be required to provide information to in-scope companies.

The Proposal clarifies that the suspension of business relationships will become a measure of last resort. Such continuity of the adverse impact relationship will not trigger liability if there is a prevention plan to address the identified issues and the company can reasonably expect it to be effective.

Moreover, where the due diligence assessment has to be performed annually in the original CS3D, the amended one will only require an adequacy assessment every 5 years.

Lastly, the limits the scope of the CSDDD to:

- EU companies with more than 5,000 employees and €1.5 billion net turnover, and

- Non-EU companies with over €1.5 billion in EU net turnover.

The Omnibus also extends the transposition deadline for Member States from July 2026 to July 2027.

What to do now?

To provide you with some political context, there were contrasting views on whether this Omnibus was even necessary and, if so, to what extent should the disclosures be reduced. Groups of companies, organisations and investors have raised their voices against the Omnibus, setting the stage for intense political negotiations and trade-offs that were not successful but raised the alarm among investors and customers.

Most companies over 500 employees were already working toward releasing their first CSRD report in 2025, and those over 250 employees, preparing for the following year. In view of these changes, those companies are now out of scope. This might be the chance to voluntarily focus on the most strategic elements od the directive, like double materiality assessments (DMA) and gap analyses. These processes have proven to remain valuable from a risk management perspective. Furthermore, the Omnibus points at the VSME framework as an alternative solution to the ESRS, so those companies could also consider to continue reporting under different standards.

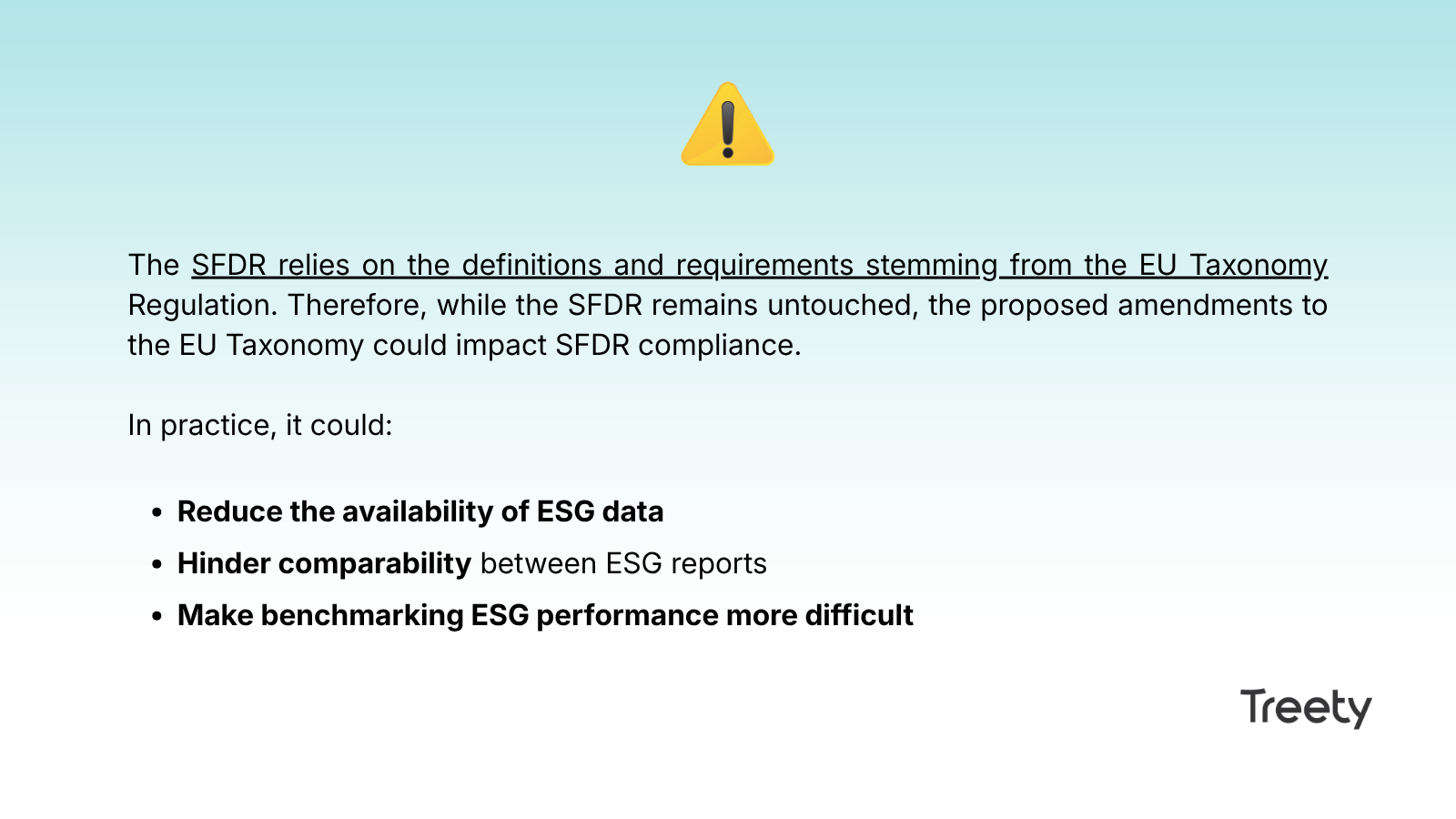

As for the changes to the EU Taxonomy, the SFDR relies on the definitions and requirements stemming from the EU Taxonomy Regulation. Therefore, while the SFDR remains untouched, the proposed amendments to the EU Taxonomy could impact SFDR compliance. In particular, it could make Article 9 compliance more accessible, given that he way to prove that the invested businesses are indeed sustainable is by disclosing their Taxonomy alignment. With the weakened criteria and the possibility to report partial alignment, Article 9 funds will find it easier to conduct such assessment and to showcase their efforts even if they are still working on attaining a few criteria.

Final Thoughts

The proposals were released with surprising speed, as such measures typically undergo extensive consultations and prolonged public debate before reaching this stage. That speed reflects the Commission‚ urgency to deregulate in response to concerns about Europe‚ perceived lack of competitiveness compared to the US and China, where businesses operate under less stringent regulations.

The Omnibus proposal suggests that increased flexibility will encourage voluntary sustainability reporting, allowing companies to differentiate themselves and attract investment. However, by lowering the bar, we risk returning to a fragmented landscape of inconsistent, self-defined ESG claims, diluting the efforts of responsible corporations into a sea of flexible (or may we call them greenwashed) ESG reports. This undermines the very purpose of the framework: ensuring that only those who truly meet sustainability criteria can claim to be sustainable and rightfully access all the benefits that come with it. Yes, compliance is demanding, but it is for a reason. Large corporations, with their resources, can bear the cost, and smaller companies would have benefitted from established best practices, clearer guidelines, and industry benchmarks when their time came.

If you are struggling to decide what to do next, we can help you find out what makes sense for your portfolio. Feel free to reach out!